Executive Summary

Over the past year, the financial advisory world has witnessed the emerging rise of the "robo-advisor" - technology-driven investment advisory services that substitute "expensive" humans for low-cost highly-scalable software and algorithms that seek to deliver much of what advisors do with respect to portfolio construction today, but at a fraction of the cost.

Underlying the robo-advisor model, though, are insights that are relevant to any financial advisory firm. For instance, the core building blocks of robo-advisors - a systematized investment process, supported by programmed technology automation to implement the portfolio - is not actually unique to robo-advisors at all. Any advisor - human or robot - can use these tools, and they already exist!

In fact, it turns out that many financial advisors already deliver everything that robo-advisors do, and more; advisory firms have been increasingly shifting to model-based portfolios for years, and "intelligent" rebalancing software that replicates virtually everything a robo-advisor already does has been around for nearly a decade, as has been shown indirectly by Morningstar's "gamma" research. Which means in the end, robo-advisors may be less of a threat to traditional advisors, than simply an acknowledgement that inefficient advisors that don't systematize and utilize technology will be increasingly threatened by those who do - whether robot, or technology-augmented human.

The Robo-Advisor Value Proposition - Systematizing And Automation

One of the key distinctions of the investment offerings provided by "robo-advisors" like Wealthfront and Betterment is that they have entirely systematized their investment approach. While this doesn't literally mean that every client will receive the exact same asset allocation and investment holdings, it does mean that every client at a given level of risk and with similar goals will have the exact same asset allocation and investing holdings.

The reason this matters is that a truly consistent and systematic investment process allows for two key efficiencies: first of all, it allows the firm to focus on a narrower set of investment decisions where small improvements can benefit everyone; and second, consistent portfolios and the technology tools to support them can automate much of the process, bringing a level of proactive efficiency to investment management that simply cannot be achieved on a one-at-a-time client-by-client basis.

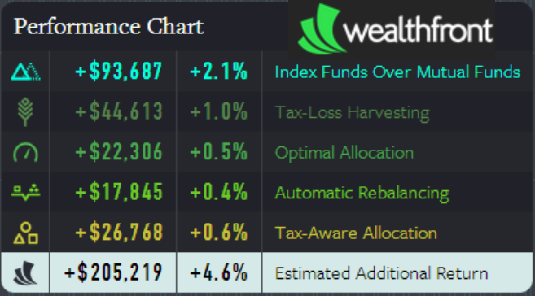

Accordingly, the chart below shows the primary "value-adds" (in percentages, and the additional dollar amount that would be accumulated from a $100,000 starting position over the span of 20 years) that Wealthfront communicates as a part of its marketing. While some might debate the particular numbers, the essential point is that Wealthfront's value-adds fall into three primary categories: managing cost (indexing over highest-cost mutual funds) and having a process to come up with the right (optimal) diversified portfolio (via their systematic investment process), automatic rebalancing, and various forms of (automated) systematic tax-sensitive implementation (e.g., loss harvesting).

Systematizing Investments With Model Portfolios

One of the primary reasons that robo-advisors enjoy such efficiencies - and are even capable of automating so much of the trading, rebalancing, and tax-harvesting process in the first place - is that their portfolio design process has been entirely systematized. In practice, many - but certainly not all - advisory firms implement portfolios similarly, though in the advisor context they are typically labeled as "model" portfolios, such that clients are allocated into one of a series of model portfolios based on their goals and risk tolerance.

Creating model portfolios allows firms to focus their research and due diligence process on a narrower range of investments - just the subset being held or considered for one of the portfolio models - and in turn makes it possible for them to spend more time per investment finding the right/best/ideal solution, whether it's about getting the lowest cost, best execution, ideal construction of the underlying investment structure, or some other feature.

In essence, having 100 portfolios for 100 clients means 100 sets of investments that require research and monitoring, while having all clients allocated to "just" 5 portfolios allows the firm to reduce its due diligence burden by 95%! In other words, having model portfolios allows the firm to gain the same efficiencies as a robo-advisor to focus on establishing the lowest-cost "most optimal" portfolio for clients.

While historically, advisors implementing a different portfolio for every client has been defended under the auspices of "we fully customize our solutions to the unique circumstances of each client," in the future such an approach will increasingly opens advisors up to the criticism that they can't possibly do an effective job continuously monitoring portfolios and performing appropriate due diligence on client investments the way a robo-advisor can. In addition, advisors open themselves up to criticism that they should just have a portfolio representing their "best ideas" and strategies, rather than having as many different investment approaches and portfolios as there are clients, which is almost impossible to all be the best ideas!

Automating Rebalancing And Tax-Savvy Decisions

Beyond the pure efficiency of investment research and due diligence, though, the real value of adopting model portfolios comes from the ability for advisors - like robo-advisors - to leverage technology for continuous monitoring of portfolios, which simply isn't possible with the same manner of efficiency when every client has a different portfolio.

In fact, while Wealthfront makes the case that a great deal of its value proposition is tied to its ability to effectively implement its continuous-monitoring automatic-rebalancing and tax-loss harvesting, the reality is that the benefit isn't actually unique to robo-advisors at all. Technology-driven automatic rebalancing, systematic tax-loss harvesting, and tax-aware asset location, have already been available to and implemented by advisors in the form of "intelligent" rebalancing software for a nearly decade now (at least, those advisors who have already implemented model portfolios!)!

However, actual advisor adoption of these "robo-advisor-equivalent" tools is still astonishingly low; the latest Financial Planning magazine Advisor Technology survey found that more than 60% of advisors still don't use any form of rebalancing software, a moderate improvement from the prior year's 69%, which has left the door wide open to a challenge from robo-advisors. Not because human advisors can't acquire and implement the technology to do it, but simply because they have lagged in technology adoption and opened up the threat to themselves.

In some cases, the blocking point is that the firm simply hasn't taken the time and made the investment into rebalancing software; in other situations, the issue is that the firm's investment process is not systematized and is still different for every client, making efficiency with rebalancing software outright impossible; and in still other situations, investment models might exist and the software might have been purchased, but it is not actually being used properly to allow for robo-advisor-like efficiency.

Human Advisors Delivering Robo-Advisor Solutions

While robo-advisors have been hailed as a rising threat to traditional human advisors, the reality is that the robo-advisor's tools of the trade - systematic model portfolios that are continuously monitored using technology to take advantage of rebalancing opportunities and tax-loss harvesting, while being implemented with low-cost investments delivered in the form of the 'optimal' portfolio matched to the client's goals and risk tolerance - are not actually unique to robo-advisors at all. Instead, they're simply the outcome of an intersection between a systematic portfolio design process, along with the savvy use of technology to implement those strategies, with tools that already exist.

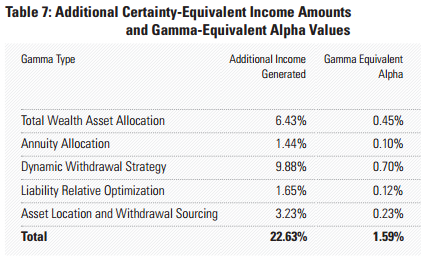

Accordingly, the reality of the advisory landscape is that many advisors already fully deliver the entire core value proposition of the robo-advisor, and have for years, by implementing a consistent range of model portfolios appropriate for client goals and based on their risk tolerance, implementing with "intelligent" rebalancing and trading tools that allow the portfolio to be continuously monitored, rebalanced as soon as it is appropriate to do so, and managed on a highly tax-sensitive basis proactive tax loss harvesting (though, notably, in today's tax environment, loss harvesting may be overvalued, or even harmful in some client circumstances!). In fact, ironically the Wealthfront robo-advisor value proposition is remarkably similar to the benefits articulated by Morningstar researchers as the "gamma" that human advisors already bring to the table!

Of course, this balance of generating gamma by implementing systematized portfolios while heavily leveraged technology to automatic rebalancing and loss harvesting isn't meant to undermine any of the other value propositions that advisors bring to the table with their financial planning and wealth management services. In fact, it makes the point that as is, the primary difference in pricing between robo-advisors at 25bps and the "typical" advisor 1% AUM fee may be less that about the idea that advisors "cost more" than robo-advisors but instead because they deliver (everything and) more for a commensurate cost. On the other hand, the robo-advisor trend is commoditizing the core management of a passive strategic diversified portfolio, forcing advisors to ensure that they meet the "robo-advisor minimum standard" and bring more value to the table for clients as well.

Nonetheless, the reality is that even with the available tools, clearly not all advisors are delivering what robo-advisors do today; as noted earlier, only 40% of advisors are even using some form of rebalancing software, and for many the blocking point is not just a failure to invest in technology, but a failure to systematize their investment process into model portfolios that would even make rebalancing software feasible and really effective in the first place. For those advisors, the robo-advisor is a dangerous and emerging threat, as robo-advisors deliver similar or better solutions at a lower cost, while those advisors have limited time and capacity to deliver more value-adds while they're so focused inefficiently delivering the investment portfolios they already do.

But the fact remains that in today's environment, nearly all of the solutions that robo-advisors implement can be done by human advisors as well, and many have already been doing so for nearly a decade. While the robo-advisors do have some modest enhancements even beyond today's technology-augmented human advisors - for instance, Wealthfront doesn't just own a large-cap index fund, it actually buys each of the 500 stocks in the S&P 500 in appropriate weights so that it can systematically tax-loss-harvest at the individual stock level, and both Betterment and Wealthfront aggregate trades across all client accounts (since they also broker the transactions) so that they can do so without any transaction cost to clients - the power for human advisors to compete with robo-advisors lies entirely in the hands of human advisors to systematize their practices and utilize the available technology, to deliver virtually everything robo-advisors already do, and more gamma on top of it...

Give the robo-advisors credit: they spotted the low hanging fruit in existing firms’ inefficiencies (not systematizing the on boarding process, not standardizing model portfolios, and not using powerful rebalancing software), built their own algorithms to automate these processes, and then marketed the heck out of them!

So to the advisors and business owners reading: what are you doing to optimize your processes?

If you’re not moving ahead with opportunities in these key areas Michael mentioned, you’re falling behind due to the work being done by the robo-advisors.

Michael, great job wrt laying out the tactical issue(s). I would add two other variables: 1) pricing and 2) the actual technology. Both SigFig and WiseBanyan have effectively introduced the Freemium model for pricing. But what should advisors be thinking about wrt the actual technology? Is this where providers like eMoney and MoneyGuidePro should really be stepping in?

So the take away is that the difference between a robo-advisor and a classic RIA with auto-systems under the hood is that the robo is VC-backed and has the good sense to embrace its inner bot through marketing, segmentation and pricing?

Brooke

Indeed Brooke. I’d characterize a robo-advisor as having a much clearer focus on what it does, and excelling at delivering that core value proposition with a system that’s built to scale from the start for its target market (though I think they sometimes overmarket their actual scope).

By contrast, the advisory world is notorious for being both undercapitalized (for aggressive marketing/investment/expansion), and failing to focus the value proposition around a core target market.

On the other hand, the biggest factor that has yet to play out is the VC-driven demand for return on investment. The current suite of robo-advisors can’t just be cash-flow positive or profitable alone to be a VC ‘success’. They need to be HUGE. It’s not clear whether the expectations bar set for themselves is so high that they might well “succeed” by industry standards yet “fail” by the standards of the VCs that fund them (and who ultimately control whether they’re sustained or shut down).

We’ll see…

– Michael

How do the robo-advisors (and advisors who have systematized the investment process) handle asset location? Do they locate tax-efficient strategies in only taxable accounts and tax-inefficient strategies in only tax-deferred or tax-free accounts? Or do they avoid investments that have these issues? I am thinking about managed futures, hedged equity strategies, Master Limited Partnerships, etc. I have many clients with just IRA money, just taxable money, or a mixture of the two. Can the software handle these kinds of situations?

Advisors don’t go into business saying that I want to spend 65+% of my day doing paperwork of one sort or another. Yet, that’s what happens.

Except for those who systematize and automate. They’re realizing their goals because “someone else” — a person or computer or both are in place.

S.Y.S.T.E.M.S

Save

Yourself

Stress

Time

Energy

Money and be more

Successful!

To Bill and Michael, how do you see this level of portfolio management efficiency applied when advisors are integrating held-away assets such as 401k plans into client portfolios? Thanks

What free or inexpensive tech tools (or non-tech resources) would you recommend for a newbie, to help with client presentations (illustrating how financial products work / potential / pros / cons) and for organizing my own work / business?

My sense is that some of the best tech tools for financial professionals come with a significant price-tag. As a rookie (since 2014) Insurance Agent and Registered Rep, I’m not ready to invest much towards technology.

I am a consultant in one of the loan companies in Poland and was wondering how to do it?

I am a manager in one of the loan polish companies and i know it’s not easy process for sure 🙂