Executive Summary

Financial planning is hard work. It's hard work for the clients, who must spend far more time than they are accustomed in the process of digging through their personal financial lives and their goals. It's also hard work for the financial planner, who invests an incredible amount of time into the process of creating a financial plan for the client, entering client data into financial planning software, "crunching" the numbers, and then crafting a written plan to explain and justify the results and the associated recommendations. Yet as planning software becomes increasingly more complex, we are approaching a difficult crossroads: the depth of the planning software requires more and more time to do the analysis, and necessitates more and more written detail to support the software output. As a result, the planning process itself drags out, taking hours and hours to create a plan and weeks and weeks to deliver recommendations to clients. But when did the complexity of financial planning software begin to drive the planning process, instead of being a tool to expedite it? Has our financial planning software become the enemy that's ruining our productivity, instead of improving it?

The inspiration for today's blog post is a recent study released by the FPA on the fees that financial planners charge for their services (which was just highlighted in my Weekend Reading column). What was notable in the study, though, was not just the fees that financial planners charge for their services, but the time it takes for them to actually use financial planning software to complete a written financial plan.

How Long Does It Take To Create A Financial Plan?

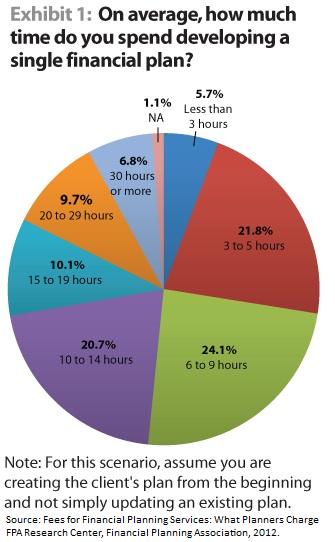

As the figure shows, while a quarter of financial plans take a relatively modest 3-5 hours or less, another quarter of them take 6-9 hours, while nearly 50% of all plans take 10+ hours, including almost 30% of plans that take more than 15 hours! All to develop a single financial plan! And while I will grant that for a small subset of firms, their typical client is so affluent and complex that it requires extensive analysis time, I have to question overall if it's really true that 50% of all financial planning clients have situations so complex that even a full-time professional financial planning expert needs 10+ hours to figure out what to do!

As the figure shows, while a quarter of financial plans take a relatively modest 3-5 hours or less, another quarter of them take 6-9 hours, while nearly 50% of all plans take 10+ hours, including almost 30% of plans that take more than 15 hours! All to develop a single financial plan! And while I will grant that for a small subset of firms, their typical client is so affluent and complex that it requires extensive analysis time, I have to question overall if it's really true that 50% of all financial planning clients have situations so complex that even a full-time professional financial planning expert needs 10+ hours to figure out what to do!

Moreover, the arduous time to complete the financial plan also stretches out the timeline for turning around the plan to the client. The FPA study also revealed that only a quarter of planners actually deliver the written financial plan less than two weeks after the initial discovery meeting (which, coincidentally, is about the percentage of planners who take no more than 5 hours to complete a plan); the remaining 75% of planners take at least two weeks to deliver the plan back to the client!

All of which raises the question - what is it we're doing that takes SO long, and do we really NEED to do it that way? In my own experience, a large portion of the time necessary for plan construction from the FPA research is in fact attributable not just to the process of analyzing the client's situation and crafting recommendations, but in using our financial planning software to support the actual creation of the written financial plan. Yet as I've written previously, it's already a little unclear why it is we as planners spend so much time building financial plans when we all acknowledge that virtually no one actually reads them.

Is Financial Planning Software Too Complex?

It appears to me that we have created a difficult circular problem for ourselves as financial planners. It takes time to do the analysis for a financial plan, in no small part because of the complexity of our software. So we gather our client data, and disappear for a week or two to work through the software and craft a plan. But we can't just come back with a brief list of client recommendations on a single piece of paper, because clients won't trust it and act on it after we've been off with our black-box software for so long. So we need to justify our recommendations by providing a written plan to support the software output. But the thoroughness of the written plan - even if only to serve as a trust-building exercise - in turn requires so much time, it drags the process out even further, and the plan takes still longer. And heaven forbid the client has a question we failed to cover in the initial version of the plan... then we tell them to come back in another two weeks while we run the updated information through the software again!

Is there a way to get off this productivity-destroying roller coaster? I believe there is. The solution is to give clients a more interactive planning experience, where much of the planning "work" is done live, on the spot, with a screen showing a plan that the client can manipulate, with the planner sitting nearby acting as navigator and guide for the process. Anything the client wants in written form is simply printed at the end of the meeting itself. If the client needs any educational materials for a specific issue, those can be delivered too, at the time. But the rest of the written plan disappears as unnecessary.

Because simply put, the client doesn't need a giant written financial plan when the client was a part of the plan construction process itself, and can kick the tires and take the plan for a test drive and make a final decision on the spot. In other words, with a more interactive planning experience, the client gets buy-in to the plan and an outcome that can be trusted, because the client has become part of the building process in the first place. In this context, financial planning software that supports a real-time collaborative and interactive client experience returns to its rightful place as an enhancer of productivity, not a detractor.

There's just one real problem. We don't really have financial planning software that is up to the task. At least, not yet. But it may not be far off, with an array of new financial planning software offerings coming to the industry lately. Can you imagine the experience for the client, not to mention the efficiency of your practice, if the bulk of the planning really could be done in a 2-hour meeting with software that effectively supports the process... cutting out not just a dozen hours of written plan construction, but a 2+ week delay as well?

So what do you think? If there was a financial planning software package that was so easy to use, it could analyze a client's situation on the spot, would you use it? Would your clients engage (more) in the process? Could it make your practice more efficient? Have we unwittingly held our own financial planning process hostage to the limitations of our software, instead of using the software to enhance our financial planning productivity?

Before software was created to make plans, everything was done manually. The only option planners had was to gather information, disappear for a few weeks, and then propose the completed plan with a few alternatives.

Today, software allows for a much more rapid turnaround. Perhaps some planners feel guilty for turning a plan around so quickly, yet still charging many thousands of dollars for the engagement.

For me, the planning profession ought to embrace the Dr. Lazenby approach of real-time, interactive, and “fun” planning engagements. Disappearing for weeks on end is a terrific way for planners to distance themselves from Gen X/Y.

Michael/Bill,

Interesting piece and comments by Bill..

I can’t agree more..

I have been checking out financial planning software for a very long time and finally I do find that ‘Figlo’ can come pretty close to what you are visualizing, specifically for the Gen X. I have been experimenting it and its easy GUI makes it fun and one can do plans pretty quickly. You can ask for trial version and check it out..However, a word of caution.. They still have to work on some localization issues before they get ahead.

But overall, I think ‘Figlo’ can be a game changer, specifically focused on mass affluent/Gen X clients. Imagine running it on ipad and getting the client involve in the financial planning process across the table along with ‘what if’ scenarios etc. Or for that matter give the client the access to play around and do their own plan quickly. It seems to be possible with ‘Figlo’!!

P.S.: oops ..this comment got posted as anonymous.. Apologies!

Hi Michael

Yes, No, It depends.

Agreed- interative and collaboratively self-determined creates buy-in

Agreed- a need for greater efficiency (likely driven by the need for speed in a “I want it now culture”)

would the interactive planning software solve all their financial planning needs, concerns, behaviors?

Maybe, maybe not

Is trust and confidence in a plan cemented because of new technology and speed? A collaborative black box where “assumptions” build confidence?

it seems that financial plans crystalize dialogues and conversations with clients regarding their values and life situational issues, concerns and the contextual meaning for their money and their lives

a 2 hour meeting will collaboratively crystalize all of this? I wonder?

Two things. First a few things that I find suck up an undo amount of time when trying to perform quick plans for people. Than a rant on financial planning software.

———–

* Analyzing 401K investment options – Every plan is a snowflake with different combinations of funds available. To make things worse, there are so many versions of the same funds (with different expenses) that you have to double check them all before making your recommendations.

* Integrating 401K investment options with the rest of the portfolio – Since the investment 401K investment universe is constrained you must work around it for the rest of the investments.

* Deciding when and how to take defined pension benefits – While these are slowly disappearing, each plan has different rules for retirement, with different amounts at different times, different survivor benefit options and health insurance implications.

* Analyzing variable annuity contracts – Everything is hidden in the small print of the prospectus. Reading these and analyzing under what scenarios they are good and bad takes time.

* Analyzing private REITs, Oil drilling, etc. More crazy prospectus’ and other due diligence work. You would think these would be limited to high net worth individuals, but I keep finding these being sold down market as well.

———-

Financial planning software goes deep in all the wrong places.

Misleading precision – ignoring the variability in returns for a moment, just how accurate are those projection of income, expenses and taxes. I would argue there is a ton of variability there that swamps out the detailed answers the software tries to project.

Lack of relevant output – what is with these percentage of success metrics. That is not how people think or how it will play out. People tend to care more about understanding the range of outcomes and potential trade-offs rather than the percentage chance of a particular outcome.

Ignores P&C risk – There is all this great data out there about how likely your car is to get into an accident, your house to burn down, etc. Why doesn’t financial planning software run scenarios where these bad things happen to see whether current insurance coverage’s are sufficient.

I could go on, but it is too depressing.

———-

So, yes financial planning software is broken. It needs to be more interactive, properly model uncertainty in the inputs and help clients actually focus on the right things.

But that is not enough. We also need our pension systems to become standardized (e.g., make all 401Ks portable like IRAs).

I am not sure how to solve the complex product problem (e.g., annuities, private reits, etc) though other than regulate them like prescription drugs (e.g., you need a non-commissioned planner to write you a prescription to buy them). Vanilla/standardized versions of these products could be sold directly to the public.

Enough ranting for today.

David

Hi Michael

Truth Financial Planning Software in the UK does just that. You do the planning WITH the client. No need to print long winded plans that clients never read.

It takes 30 minutes to build a plan. That’s it. It might take 1-5 hours to get the data from all the different product providers / and or client, but creating a detailed MEANINGFUL plan is straightforward. And clients love it. And every year it is a case of revisiting the Financial Plan, WITH the client, and helping them stay on course / correct course. That means Advisers / Planners don’t have to talk about products / performance or fund switching to justify their existence (a lot of that is going on in the UK).

Outstanding article Michael. I’ve been doing scenario analysis one on one with the clients in Naviplan.

One client even said “you make financial planning fun!” While not my goal, the clients become engaged and seem to get a better ownership and understanding of what they need to do. After all and what I make sure they understand, they have the hard part.

Plus, they get a say on the final inputs, and can digest the sacrifices and decisions around what goals can be reasonable achieved.

We spend a lot of time together in the analysis meeting, after I’ve been behind the wall for a couple hours of course to get things prepped. But then we have our conclusions and next steps, plus an understanding and often better communication between couples.

Finally, I don’t think we can predict every possibility with 100% accuracy. But we tell the clients that, and give them greater visibility of their risks so they can decide how aggressively they want to mitigate, and of course we try to review regularly and adjust.

Thanks,

Tom

Couldn’t agree more, Michael.

For these reasons I use MoneyTree Silver planning software. Very straightforward, fast entry, etc. Works well for my typical mass affluent, second-half-of-life clientele.

At the conclusion of the initial interview, I collect the client’s actual documents (no canned questionnaires) for analysis and data entry. Though clients may be focused on retirement projections, I also review their tax, estate, and risk management/insurance matters.

There is generally only one follow-up meeting and that can be scheduled shortly thereafter. At the meeting, the client and I interactively walk through issues/assumptions on my laptop computer. This walk-through seems to give them greater understanding and buy-in. And we make on-the-spot changes and review “what-if” scenarios right there.

With this approach, it seems the client better recognizes the value of “the planning” rather than “the plan.” So it’s not the software output that they’re paying for per se, but the advice and understanding shed along the way as we interactively walk through it.

No “plan” is produced until we’ve gone through this process together, discussed my findings/concerns, and they’ve provided additional input.

Then I write a summary/recap of key issues and recommendations and, instead of a telephone book sized document, I attach about 8 pages of charts/assumptions. Most of my clients are happy to receive this in pdf format via email instead of me mailing hard copy.

Using MoneyTree Silver’s simpler software and taking this approach has made it possible for me to provide a thorough review, yet not spend near the time shown in the FPA survey.

Hi Michael

I have only ever used Truth Financial Planning Software. The biggest delay I have is getting the relevant information back off the client. The plan itself only takes a couple of hours.

All plans are then presented on a flat screen tv and we work with the client on their plan. The client can see the effect that any particular change will have on their cashflows or how much they can spend on holidays etc.

We do this exercise annually to reflect any changes and keep them on course.

When the meeting is finished and we have agreed on assumptions and a course of action, I will do up minutes of the meeting and print off a summary plan for them. This is mainly charts and graphs.

Hi Michael/Everyone,

I am a financial counselor on a military base. I work primarily with military members, wounded warriors, DoD civilians, DoD contractors and the family members of all the above.

I appreciate this topic greatly.

The government has supplied me and my colleagues with a great excel spreadsheet for detailed cash flow management. It is very eye opening for many but that is all it can do is cash flow.

I meet with many clients at or near retirement or separation from military or federal employment. I’ve been able to hobble together information and a hodge-podge of websites to help them think about comprehensive planning, but this is patchwork.

Do any of you have recommendations of websites that can be used to put together a decent/starter plan?

Some caveats:

1. It needs to be free (no likely funding for software due to budget constraints)

2. It needs to be accessible from highly monitored and restricted computers (military security, restrictions and firewalls)

It is my deepest hope that if I can interactively address the topic, as Michael suggests, my clients’ eyes will be opened to the need for comprehensive financial planning. Then they can seek appropriate service from professionals such as yourselves.

I am grateful for any and all input that will help me serve those who serve us.

Thank you.

Lee Acker

[email protected]

Hi Michael,

As a financial planner based in the UK I spent years wrestling with these issues, as a result we built;

mylifecash – http://www.youtube.com/watch?v=0b0jBMSFg6c

lifecashpro – http://www.youtube.com/watch?v=GiQ8o_8Ne2k

We decided to give financial planning the Apple user experience. The lite version is now available in the USA.

I look forward to your thoughts on developing the Pro version for the USA/Canadian markets.

Thanks,

Nigel

Nigel Burgess

Lifecash Limited

Thanks for the great article. Currently I am looking at all different software programs Naviplan, MoneyGuidePro, MoneyTreeSilver, and Masterplan.

The further I get into looking at the software it seems they are more geared to sales of either stock or insurance than looking at the whole picture. I am almost to the point of wanting to start developing my own software.

Michael,

There is planning software – VisionWorks – that’s been intentionally designed for interactive use WITH client. Currently, it’s available only in Canada. We’ll be starting the U.S. version shortly. And you’re right. Most of the issues that you raise can be overcome, when you create a plan WITH clients.

It’s our belief that the “Six-Step Process” and the notion that plans should be created FOR clients is outdated. It was necessary 25 years ago, when the state of technology was very crude. Advisors had to create plans and then assemble their recommendations in a presentable document for delivery to clients.

But creating plans FOR clients was never the preferred way to plan. The purpose of planning is not the creation of a plan document – it’s learning, decision making, and action. Adult learning principles stress that adults don’t like to be told what to do. We prefer to understand the implications of our options and make our own decisions. With our life-planning approach, learning happens through the conversation you have WITH clients as you model “What if?” scenarios in the VisionWorks life-planning software.

When clients see the long-term implications of their options, they learn and make decisions for themselves. Action then follows naturally.

Further, plans created for clients never satisfy them, because they never suit their preferences – no one can ever make values-based lifestyle decisions for someone else.

If you’d like to learn more about VisionWorks, there’s a Quick Tour video on the Home page at http://www.visionsystemscorp.com.

Michael Curtis

416-421-2431

888-578-3247

Excellent read. Thanks for sharing. Investing in financial planning software has become a need more than a want nowadays. If we want our finance team to spend less time on administrative chores and more time actually analyzing and planning as well as engaging in continuing education, then having a business budget planning software in place is definitely a must. Read related articles at http://www.performancecanvas.com/resources/blog/