Executive Summary

While the current low-yield environment has presented significant challenges to retirees trying to generate retirement income, the upside is that low yields have also driven down borrowing costs to record lows. As a result, retirees are increasingly deciding that perhaps keeping a mortgage and not paying it off is a good idea after all; with the average long-term return on stocks being significantly higher than today's 30-year mortgage rates, an inexpensive mortgage becomes a strategy to leverage the household balance sheet and boost the amount and sustainability of retirement income.

Yet the decision to keep a mortgage in retirement is not without risk. There's a danger than equities won't perform as expected, and fail to generate a return in excess of the borrowing cost over a relevant time period. And even if the returns do ultimately add up, the ongoing payment obligations for a traditional mortgage create a "sequence of returns" risk for the retiree, where withdrawals to handle the mortgage payments could so deplete the portfolio during an extended period of bad returns that there may not be enough money left over for when the good returns finally arrive.

From this perspective, retirees should perhaps consider the reverse mortgage instead. While such loans have been relatively unpopular - due in part to their high costs, and because they're often viewed as a borrowing option of last resort - the reality is that the lack of any cash flow obligations for a reverse mortgage actually allows it to eliminate the sequence risk from the mortgage-in-retirement strategy. In fact, over a long period of time, using a reverse mortgage in retirement can result in materially greater wealth when equities do perform as desired, as the reverse mortgage maintains a greater amount of household leverage, even while reducing the exposure to the impact of an unfavorable sequence of returns.

In the end, there are still a few caveats to the strategy - most notably, that reverse mortgages still tend to have higher upfront and ongoing borrowing costs (though the gap is narrowing), and that lending limits may constrain the usefulness of the strategy for affluent clients (who are often most interested in increasing household leverage as a retirement strategy). Nonetheless, the fact remains that for those who truly do wish to engage in the mortgage-in-retirement strategy, the reverse mortgage may be the most effective way to execute it.

Keeping A Mortgage In Retirement

In today's low yield environment, it has become increasingly popular for retirees to maintain a mortgage in retirement, especially more affluent retirees who also have an invested portfolio. The logic is relatively straightforward: when borrowing rates are as low as 3.5% to 4.5% (as they have been in recent years), and the long-term return of equities is significantly higher, why not borrow at a low rate of return to pursue a higher one? Especially given that the mortgage interest is potentially deductible at ordinary income rates, while the growth in equities may be primarily taxed at preferential long-term capital gains (and qualified dividend) tax rates.

Of course, the primary caveat of the strategy is that there is still a risk that equities will not outperform the borrowing cost over the time period, or at least that the expected return premium of equities over today's mortgage rates isn't worth the risk. With a potentially depressed equity risk premium in the coming years given today's high Shiller P/E10 ratios, is it really worthwhile to borrow at a 4% rate if the expected return might only be 3% to 4% real (6% to 7% assuming modest inflation), generating substantially less potential reward than the historical equity risk premium given that paying off a mortgage is effectively a risk-free return?

Certainly, the longer the time horizon, the greater the likelihood that equity growth eventually lifts the portfolio return above the cost of the mortgage. Yet at the same time, a longer time period can also magnify the shortfall if an unfavorable return sequence occurs, especially since the reality is that ongoing payments into the mortgage do introduce an aspect of sequence risk to the analysis. In a similar manner to taking withdrawals for retirement spending, there's a danger that ongoing amortizing mortgage payments will deplete the portfolio enough that by the time the good returns finally arrive, there's too little left in the portfolio to make the subsequent growth enough to outweigh the cash flow obligations of the remaining mortgage payments.

Whether the withdrawals from the portfolio go directly to pay down the mortgage, or other fixed income cash flows pay the mortgage - but thereby aren't invested into the portfolio for growth - the end result is the same: keeping an amortizing mortgage and a portfolio creates a sequence-of-return risk for the retiree, such that even if the long-term return averages out favorable, the retiree may not finish with more money.

Amortizing Vs Reverse Mortgage

Of course, the reality is that retirees don't have to use an amortizing mortgage in retirement. While such mortgages are the most common, those who want to minimize the exposure to sequence risk could choose one with smaller cash flow obligations. For instance, an interest-only mortgage would have less exposure to sequence risk than a fully amortizing mortgage. In theory, the ideal solution would actually be a negative amortizing loan, with no cash flow obligations whatsoever; unfortunately, though, the options for negative amortization mortgages are close to none since the 2008 financial crisis.

The notable exception, however, is the reverse mortgage, which in fact is a negative amortization mortgage, as it has no cash flow obligations and allows interest to simply accumulate and compound against the mortgage balance indefinitely (or at least, as long as the borrower is alive, keeps the property as a primary residence, maintains reasonable upkeep, and pays the requisite property taxes and homeowner's insurance). Accordingly, the reverse mortgage actually represents a unique opportunity to maintain a mortgage in retirement, while alleviating the cash flow obligations that trigger a sequence risk to the strategy.

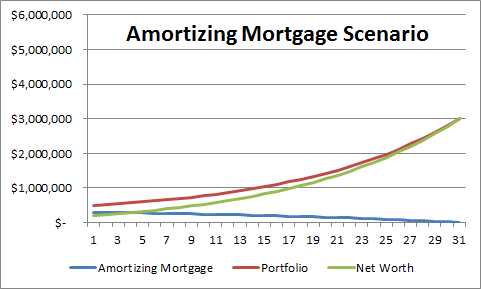

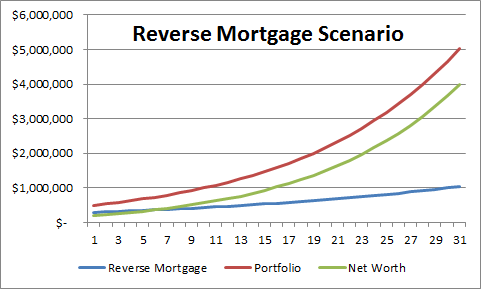

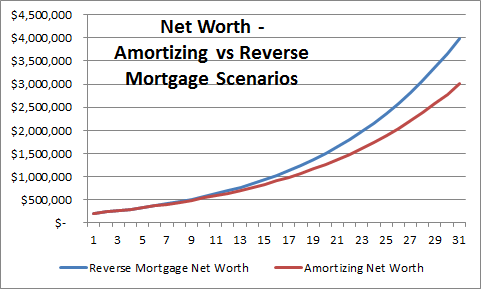

In fact, the reverse mortgage not only removes sequence risk, but for the retiree who wants to effectively buy stocks "on mortgage" with leverage, the reverse mortgage maximizes the leverage potential, as the principal payments of a traditional amortizing mortgage wind down the exact leverage that the mortgage-in-retirement strategy was intended to maintain. Accordingly, the series of charts below shows the difference over time between maintaining a $500,000 portfolio and a $300,000 reverse mortgage, versus a $500,000 portfolio and a $300,000 traditional amortizing 30-year mortgage (assuming a 4.25% interest rate on each, and an 8% average annual growth rate on the portfolio, and of course both scenarios would also have the real estate itself at whatever value it grew to). Notably, due to the sustained leverage, the reverse mortgage scenario ends out producing a significantly larger mortgage balance at the end, but a significantly higher net worth as well, as the full amount of the portfolio stays invested throughout. And it does so without the cash-flow sequence risk of the traditional portfolio.

Caveats And Implications For Financial Planners

While the benefits of the reverse mortgage are compelling for those who wish to maintain a mortgage in retirement (for the purposes of leveraging their overall returns), there are a few important caveats.

The first is that the examples above ignore the closing costs of the respective mortgages (where the reverse mortgage tends to be slightly higher, though the costs are closer for those using HECM Saver loans), and it also assumes that the interest rates will be the same for both (though given the 1.25% mortgage insurance premium on reverse mortgages, in addition to the underlying interest rate, in practice the costs don't always line up). However, given the compounded difference over the 30 year time horizon is upwards of $1,000,000 for what started out as only a $300,000 mortgage, relatively modest differences in cost will not likely undermine these results. In addition, this analysis still does not directly model the impact of the sequence risk on the amortizing versus reverse mortgage (the projections are based on a straight line), which may lead the reverse mortgage to have a higher likelihood of being the successful strategy even if it also has a slightly higher cost.

The second caveat is that the scenarios illustrated rely on both interest rates being fixed, even though many reverse mortgages are issued on a variable rate basis; in fact, with the monthly payments or line of credit option, it's required. However, even though the fixed-rate HECM Standard was eliminated earlier this year, borrowers can still obtain a fixed-rate HECM Saver loan at relatively appealing rates. The constraint of the HECM Saver is simply that the maximum borrowing limits are lower. Although in point of fact, given this strategy is most popular with higher-income and wealthier households - who also tend to have more expensive homes - the lending limits will constrain the amount of household leverage retirees can utilize, as HECM Saver loans often allow the borrower to extract no more than about 30% to 50% of the home (depending upon age and interest rates), and the value of the home for purposes of the loan calculation is capped at a Maximum Claim Amount of $625,500 (in 2013).

In addition, there is a risk to the overall household leverage strategy: that the time horizon will not necessarily last for 30 years. In the event the retiree passes away, the investment-versus-borrowing time horizon may be cut short, as will a change in life circumstances that leads the retiree to relocate and sell the house. However, for the most part these risks pertain to both the amortizing and reverse mortgage scenarios, and the fact remains that the amortizing traditional mortgage retains the greater sequence risk. On the other hand, with a traditional mortgage, the retiree could relocate and keep the original house as rental or investment property, while the reverse mortgage would require a payoff in such a scenario (as the retiree would cease to use the properly as a primary residence, one of the key requirements for keeping a reverse mortgage in place).

Notwithstanding these caveats, though, the fact remains that all else being equal, traditional amortizing mortgages introduce additional sequence risks to the household leverage scenario (above and beyond just the risk that the portfolio fails to outperform the loan) that reverse mortgages alleviate, which should make reverse mortgages especially appealing for retirees who believe it's worth the risk of maintaining a mortgage and a portfolio side by side in retirement. This can be relevant for retirees trying to decide how to finance the purchase of a retirement home (considering a HECM-for-purchase loan instead of a traditional mortgage), or even retirees who want to keep an existing mortgage into retirement but may wish to refinance it into a reverse mortgage type instead (at least if feasible within the reverse mortgage borrowing limits). Thus, while reverse mortgages have typically been viewed primarily as a "loan of last resort" for those who have entirely depleted their other assets, the reality is that reverse mortgage strategies should perhaps receive much greater consideration in the earlier stages of an affluent retirement plan.

On the other hand, given the reverse mortgage changes soon to be implemented by HUD, the reality is that the strategy may become somewhat less appealing as the upfront Mortgage Insurance Premium (MIP) costs rise. The issue will be especially severe for those who carry a significant mortgage (as a percentage of the home value) in retirement, who will be subject to the new 2.5% upfront MIP on the entire appraised value of the property (and even for those whose reverse mortgage financing would be less than 60% of the Principal Limit Factor, the new upfront MIP will be 0.5%). Of course, given that the new rules will not be implemented until the end of the month, a narrow time window remains for those who may wish to refinance into a reverse mortgage at today's more favorable costs.

Very well written Michael, wonder who got to you first, a reverse mortgage loan officer or research you did for a client? Anyway, something to add, a 70 year old in a home valued over $625,500 could gain access to over $360,000 before new rules go into effect and probably about 15-18% less after October 1st. Is $300,000 real money in the investment world from your perspective? That’s about where your bottom graph started. Very promising if you can have that conversation with the right client.

Thanks for the write up Michael – we rolled out a simple tool to help people research using home equity as part of their retirement plan. We link to some recent articles in the Journal of Financial Planning and the Wall Street Journal.

https://www.newretirement.com/Services/home-equity-solution-finder-research-4opt-Lv1.aspx

Nice work Micheal.This will help people to think about home equity after their retirement.

financial adviser Maryland

Great read, Michael. Reverse mortgages can be ideal for those who qualify for it and need it. Consumers can check out http://www.reversemortgage-blog.com for more related information.

Helpful post

A great comparison Michael. The reverse mortgage option is similar to risk transfer in some aspects – in this case the risk is transferred to the government insurance component of reverse mortgages. The real question, if these become widely popular, is the systemic risk to the system where the liability of the program (total reverse mortgage outstanding value nationally) exceeds underlying asset value of the total real estate; hence, government bailout of the difference. Thus similar to the systemic ability of insurance companies, which you discussed in your blog about risk transfer vs risk retention, to continue to fund income streams during less than optimal markets over longer than expected periods.

Reverse mortgages do appear to be valuable in that they are a tool to access wealth for income purposes. But when might this systemic tipping point arrive? Yes, hard to imagine, but then so was the mortgage meltdown in the 2000’s during it’s early stages.