Executive Summary

As 2014 approaches, the new health insurance exchanges will begin their open enrollment, and along with the new exchanges will come the premium assistance tax credit, intended to make health insurance purchased on an exchange more affordable for the "lower income" - which is actually broadly defined to include everyone up to 400% of the Federal Poverty Level. As income rises, the premium assistance tax credit is slowly phased out, until eventually it provides no benefit at all.

However, the reality is that because the premium assistance tax credit phases out as income rises, it indirectly serves as a surtax that triggers higher marginal tax rates for those who are phasing the credit out. And the marginal impact is actually quite significant; at relatively modest levels of gross income from $25,000 to $50,000 of income, the premium assistance tax credit effectively doubles the marginal tax rate (to more than 30%) for those who are purchasing health insurance from the individual exchange. For older households that are claiming Social Security early, but still obtaining health insurance from an exchange (as they're not eligible for Medicare yet), the effect can be even more severe, as marginal tax brackets, the phaseout of the premium assistance tax credit, and the phasein of Social Security taxability all overlap.

The end result doesn't mean that it's a good idea to avoid generating income - the marginal tax rates are significantly higher than just the individual's tax bracket, but nowhere near 100% tax rates. Nonetheless, the introduction of the premium assistance tax credit may mean a whole new level of in-depth year-to-year tax planning for those with relatively modest incomes, who can be subject to surprisingly high marginal tax rates under the new rules.

Understanding The Premium Assistance Tax Credit

The Premium Assistance Tax Credit (PATC), established under IRC Section 36B as a part of the Affordable Care Act, takes effect in 2014, and is intended to help make health insurance more affordable by providing a tax credit to subsidize the cost of insurance for “lower” income individuals who purchase health insurance from one of the new state insurance exchanges (the PATC does not apply for employer-provided health insurance). For the premium assistance tax credit, “lower” income is defined as those households that earn less than 400% of the Federal Poverty Level (FPL). The Federal Poverty Level thresholds are adjusted for inflation each year, and are determined based on the number of people in the household. For example, in 2013, the FPL was $11,490 for an individual and $23,550 for a family of four, which means at least some premium assistance credit is available for households with incomes up to $45,960 for individuals and $94,200 for a family of four.

“Income” for the purposes of the premium assistance tax credit and the FPL is based on modified Adjusted Gross Income (AGI), which means AGI increased by any income not reported due to the foreign earned income or housing cost assistance exclusions, any tax-exempt interest (i.e., municipal bond income), and any Social Security benefits that were excluded from income. In other words, household income for the purposes of the credit will include all bond interest (taxable or tax-exempt), and all Social Security benefits (taxable or tax-exempt).

The amount of the PATC is based on a maximum amount of premiums that an individual or family can owe, based on their income; the PATC is whatever amount of premiums would be owed above this threshold (based on the second lowest cost Silver plan available on that individual's state insurance exchange), such that the actual out-of-pocket premium is brought down to the threshold (and the PATC covers the rest). The table below shows the PATC thresholds based on the FPL.

| Income relative to FPL: | Premiums limited to: |

|---|---|

| Up to 133% of FPL | 2% of income |

| 133% to 150% of FPL | 3% to 4% of income |

| 150% to 200% of FPL | 4% to 6.3% of income |

| 200% to 250% of FPL | 6.3% to 8.05% of income |

| 250% to 300% of FPL | 8.05% to 9.5% of income |

| 300% to 400% of FPL | 9.5% of income |

Thus, for example:

Bill is a single 35-year-old non-smoker who earns $25,000 per year. His income is 218% of the $11,490 FPL (in 2013) for a household size of 1. Accordingly, this puts him roughly midway between the 6.3% and 8.05% threshold for maximum premium; his exact threshold is 18/50ths of the way from 200% to 250% of the FPL, so his maximum premium is 18/50th of the way between 6.3% and 8.05%, which means his maximum premium is 6.93% of his $25,000 income, or $1,733/year. If the actual premium for the second lowest cost Silver plan in his state is $300/month (or $3,600 per year), Bill’s premium assistance tax credit will be $1,867 (which brings his premium down to the maximum cap of $1,733/year). Accordingly, Bill will pay $144.42/month for his health insurance, with the remaining $155.58/month covered by the premium assistance tax credit. Notably, if Bill chooses to buy a different plan besides the Silver, which may cost more or less, his premium assistance tax credit will continue to be $155.58/month, but his share of the premium will be the remainder left over (whatever that comes out to be).

How The PATC Can Boost The Marginal Tax Rate

The complication that arises with the PATC is that, because it is calculated based on income (or at least, the maximum premiums owed are calculated based on income, which indirectly means the credit is determined by income), generating more income not only creates the usual tax burden associated with income, but it can also trigger a phaseout of the PATC (at least up to 400% of the FPL, as beyond that point there is no PATC at all). For example:

Ted and Janet are a 45-year-old couple with two children, and their combined income is $50,000/year. With a $12,200 standard deduction and four $3,900 personal exemptions, their taxable income would be $22,200, putting them near the lower end of the 15% tax bracket. In addition, their income for a family of four would put them at 212% of the FPL, capping their health insurance premium at 6.72% of income, or $3,360; if the cost of a Silver plan for the family was actually $1,000/month ($12,000 per year), their premium assistance tax credit would amount to $8,640/year or $720/month, bringing their own out-of-pocket premium down to only $280/month for the family.

If the couple earned another $10,000 (rising from $50,000 to $60,000 for the year), their income would rise to 255% of the FPL, which would increase their maximum premium threshold to 8.19% x $60,000 = $4,913/year. As a result, they would be required to pay another $1,553 of health insurance premiums for the family, in addition to owing another $1,500 of taxes (at a 15% tax bracket on $10,000 of income), to a total burden of $3,053 for an extra $10,000 of income. Thus, the net effect of the changing income-related threshold for the premium assistance tax credit it to boost the couple’s marginal tax rate from 15% to a whopping 30.53%!

Notably, the interaction of income and the premium assistance tax credit does not mean the individuals and couples/families wouldn’t benefit from earning more income (the tax rate is “only” 30.53%, not greater than 100%!). It does mean, however, that the marginal tax-related burden on additional income for those below 400% of FPL is significantly greater than just their marginal tax bracket.

Marginal Tax Rate Increases At Varying Income Levels

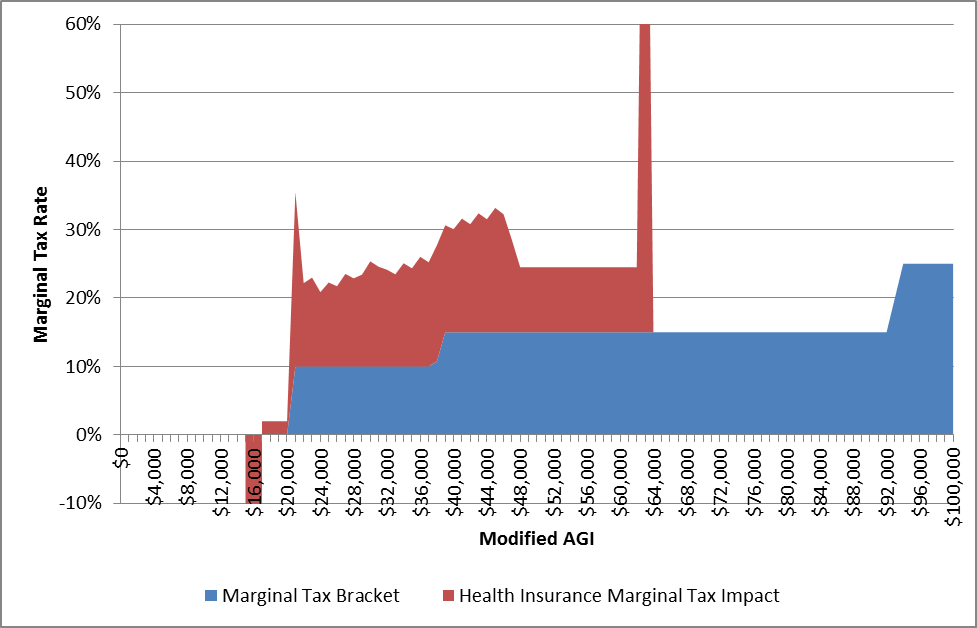

Ultimately, the impact of the PATC on someone's marginal tax rate will depend on where exactly they fall on the income spectrum (and based on their family size as well, as the FPL thresholds vary depending on the number of family members in the household). The figure below shows how the marginal tax rate of a middle-aged married couple changes as their income rises, assuming they claim a standard deduction ($12,200 in 2013), two personal exemptions ($3,900 each in 2013), and have an annual health insurance premium of $7,000 for the two of them ($583/month before premium assistance tax credits).

As the chart reveals, the impact of income of the tax credit threshold – and the higher health insurance obligation that results – leads to a more-than-doubling of the couple’s marginal tax rate. As their tax bracket rises from 0% to 10% to 15% (in blue), the tax-equivalent rate from health insurance is another 13% to 18%, resulting in a total marginal tax rate as high as 33% as the couple approaches the 300%-of-FPL threshold (which is only $46,530 of income, yet already facing a 33% tax rate!). The chart also reveals three other notable “spikes” – crossing above 100% of FPL (where the credit kicks in to begin with, essentially resulting in a favorable “negative” tax rate, assuming the couple wasn’t already eligible for Medicaid); crossing 133% of FPL, where the premium assistance threshold jumps from 2% to 3% (this is due to how the PATC tables work; from that point forward, rising income increases the threshold proportionately and not as a jump); and crossing above 400% of FPL, where the premium assistance tax credit is eliminated entirely and the couple must suddenly bear the full cost of their health insurance premiums. In this case, the maximum premium just before 400% of FPL is just under $5,900, while the full premium is $7,000, resulting in a “spike” of $1,100 of premiums for the last $1 that pushes the couple over the 400%-of-FPL threshold.

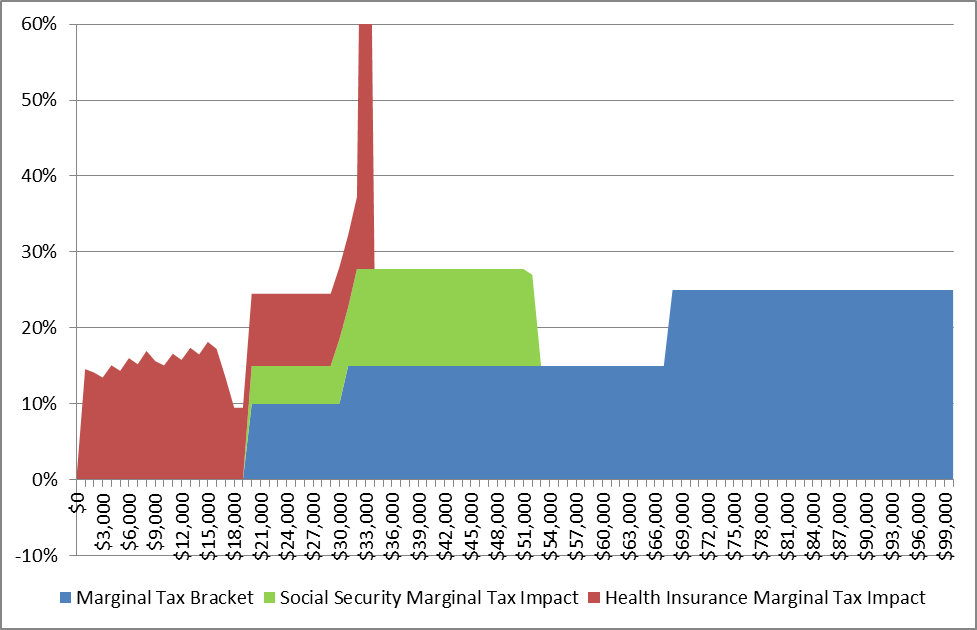

For married couples who elect Social Security benefits early – where they may be claiming Social Security but not yet be eligible for Medicare, and thus remain eligible for the PATC if they purchase their own health insurance from an exchange – the impact can be even more noticeable, as rising income can simultaneously be subject to direct taxation, trigger the phaseout of the premium assistance tax credit, and increase the amount of Social Security benefits subject to taxation. These overlapping effects are shown in the figure below, for a couple with a combined Social Security benefit of $30,000/year.

As the chart reveals, phaseout of the premium assistance tax credit begins immediately, as Social Security benefits are counted towards modified AGI to determine the couple’s “income” (even though none of it would be taxable yet, so their ordinary income tax liability would still be $0), and as income rises eventually the tax bracket, phasein of Social Security taxation, and phaseout of the premium assistance tax credit apply simultaneously. As a result, the couple faces a marginal tax rate around 15% even before they have any taxable income (i.e., before they have income in excess of the standard deduction and personal exemption), and have a combined tax bracket of 25% to 28% for most of the distance from $20,000 to $50,000+ of income (in addition to Social Security benefits). Eventually, the premium assistance tax credit has been fully phased out, and Social Security benefits taxation has been fully phased in, and the couple falls back to the 15% tax bracket for a period of time, before ultimately reaching the 25% bracket. Notably, once the couple reaches age 65 and starts on Medicare – rather than relying on health insurance exchanges and the premium assistance tax credit – the red zone shown on the chart would disappear entirely, and the couple would “only” be subject to the combined impact of their tax bracket plus the phase-in of Social Security benefits taxation.

It's also important to note that, in addition to the issues shown above, for those below the 250%-of-FPL threshold, the marginal tax rate impacts indicated above could potentially be even more severe, as the additional Federal cost-sharing subsidies (that reduce out-of-pocket obligations and the maximum annual out-of-pocket limit) are also phased out.

The bottom line, though, is simply that for couples proceeding through these “lower” income thresholds – specifically from 100% to 400% of FPL – it will be especially important to proactively manage income. In some cases, it may even be more desirable to lump income together in a single year – deliberately driving it into the 15% and even 25% tax brackets beyond 400% of FPL – to avoid having the income taxed at higher marginal tax rates in future years. Overall, year-by-year tax planning will become more important than ever for individuals and couples eligible for and claiming the premium assistance tax credit, given that all good tax planning decisions should be made based upon their marginal tax rates.

(Michael's Note: This article is an excerpt from the July/August 2013 issue of The Kitces Report. Click here for further information about this and other newsletter issues, including eligibility for CFP CE credit. Enter discount code "PATC10OFF" in the month of October for a 10% discount for new subscribers to "The Kitces Report" auto-pilot program!)

This would complicate the model, but I would love to see what the Earned Income Credit would do to the marginal tax rates…

Before people start complaining about the high marginal tax rates faced by people in the phase-out range, we should also look at the effective tax rate, which is the bottom-line tax burden. If an extra $1,000 in income takes the total tax from “very negative” to “not so negative” it is a 30% marginal rate but the bottom line total tax paid is still negative. I think a chart showing the effective rate along income lines will be very informative, if not added to this article maybe in a new article?

I disagree with the author on the foundation of this argument.

The author views the premium expense, or the lack of tax credit, as a tax. That’s incorrect. The penalty for not buying coverage, and therefore not paying premium, is a tax, but the premium itself is not.

Health insurance premiums are paid for a specific good that the individual directly benefits from. Taxes are collected by the government for the operation of the government and the general public ‘good’. That there is a tax credit that reduces some people’s premium expense does not convert the remaining premium expense into a tax.

Guest,

Higher income in this system results in less of a tax credit, which results in a greater total tax bill. I don’t know how that’s anything but a direct result of higher income resulting in higher taxes.

The premium is not the tax impact. The failure to get a premium tax credit to offset it is the tax impact. Per the example shown, Ted and Janet’s tax return would show a net liability that is $3,053 higher when they file their Form 1040 as a result of $10,000 of additional income. I don’t know how else to characterize that but a tax impact.

At $50k gross income ($22k taxable), Ted and Janet’s federal income tax before the tax credit is $2,408. After a $8,640 tax credit, their total federal income tax is -$6,232, negative six thousand. Now increasing gross income from $50k to $60k, their total federal income tax before the tax credit becomes $3,908. After a $7,087 tax credit, their total federal income tax becomes -$3,179, still negative three thousand.

Massive tax increase from negative $6,232 to negative $3,179. Extra $3,053 in tax on additional $10k in income for a 30% marginal tax rate. All true, but, this family of four making $50k pay negative six grand in federal income tax. When they make $60k they still pay negative three grand in federal income tax. That’s the bottom line.

I think our differences lie in whether the point of the article is to identify planning processes, or to comment on the social legitemacyof the benefits. The latter is better shown with a chart of the average rates (all in with premiums/discounts). The former is as shown in the article, but the conclusions should not have been in the form of “Shocking …”

There is nothing ‘bad’ about high marginal rates when support is being phased out.

I would be interested to know how contributions and w/d factor into the taxable base for the calculation for Traditional IRAs. The large premium support in years of contribution may well increase the marginal tax rate enough to make contributions much more likely to NOT create an eventual Penalty on withdrawal from an increase in tax rates.